Are you planning to set up a new company? Chances are you are a highly skilled scientist or innovator, fully dedicated to your business idea. Yet, having a brilliant idea or new product is just the first step. In order to be successful, any new business in life sciences or deep tech needs to get the essential business elements set up properly from the start.

Unfortunately, I’ve seen it happen to too many start-ups: they get excited about their innovative idea, run with it, but go bankrupt due to poor management. No matter how much you want to focus on research & development, cash is key. If you lose sight of the bigger picture and fail to monitor your cash flow correctly, you can run out of money very quickly.

So, let’s take a look at the five basic steps needed to set yourself up for success.

Step 1: Open a business bank account

The first thing to do is to register your company at the Chamber of Commerce and the Tax Office, get your registration numbers, and go to the bank. Opening a business bank account is a more rigorous process than you might think, and can take anywhere from 3 to 6 months. Organize this early on, before you really start your business processes. As soon as you need to start paying suppliers or receiving funding, your business bank account will be ready.

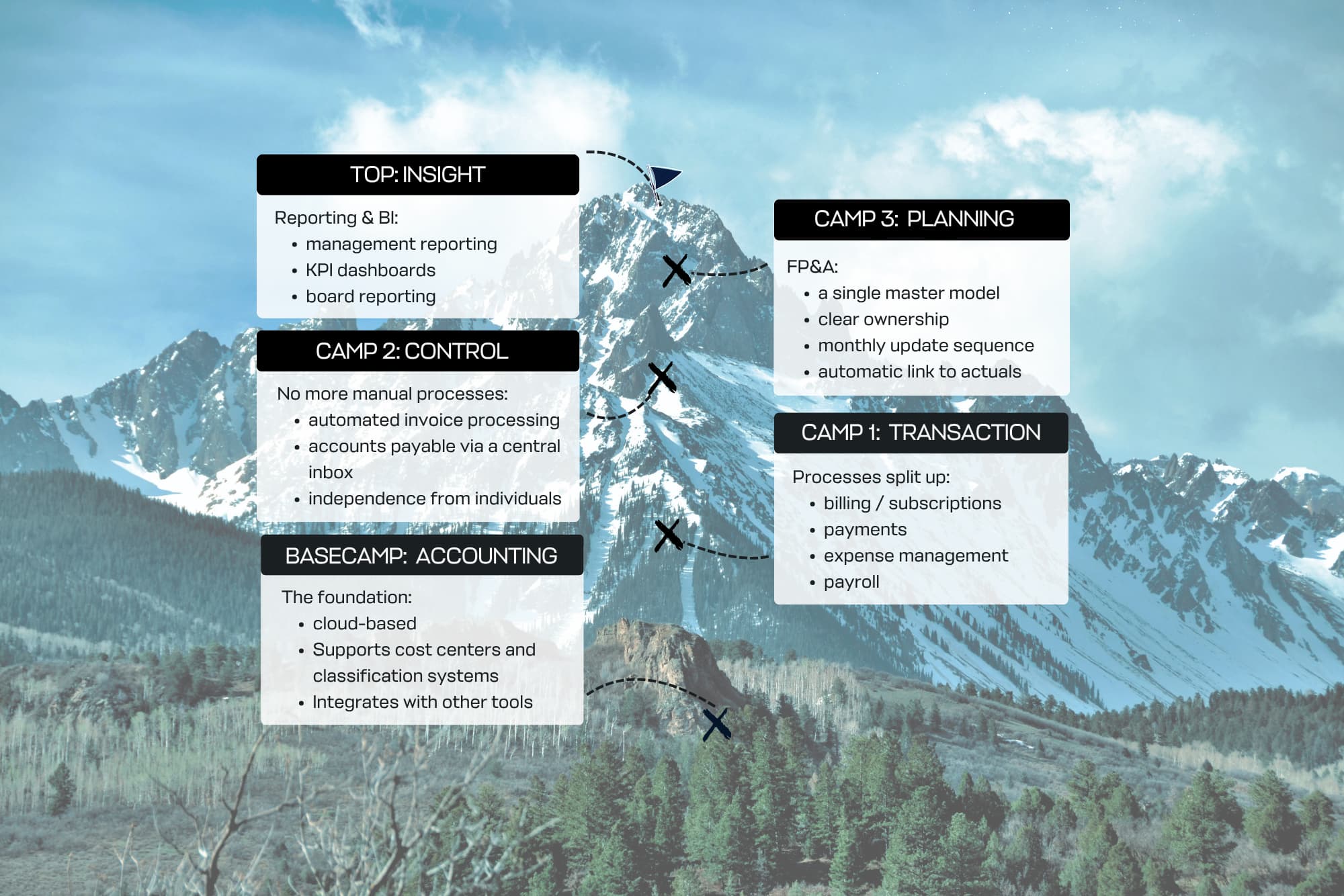

Step 2: Establish a bookkeeping and forecasting system

You may think that attracting funding depends on your business idea, but your bookkeeping system is just as critical. Investors will want to see figures early on and will challenge you on them. You need a clear and accurate overview, and you should stand by your figures and projections, or investors might lose confidence. A good bookkeeper will support you by setting up an accurate system that includes all costs, including administration, staff, office, R&D, legal costs, and registering intellectual property. Not to forget accurate tax returns, of course, to avoid fines creating unnecessary outgoings.

Step 3: Team up with a controller

Besides a bookkeeper for your administration, you might want to team up with a controller as well. By involving them in planning and control, a controller controls your financial overview and keeps a close eye on your current and future cashflow. If this isn’t set up properly, you have no real overview and in the worst case scenario you will run out of money. If you need additional funding, for example, that process needs to start 6 to 9 months in advance.

Step 4: Set up a payrolling system

Excellent staffing is crucial for your company, but realistically it is also a big cost. If you sign a contract with an employee for 50k a year, the all-in costs can add up to 80k. Your controller should be aware of all the additional costs associated with hiring an employee, such as social security, holiday leave/pay, pension scheme, or travel allowance. Once all of that is set up properly, taking all aspects into account, a payroll agency can handle the processing.

Step 5: Determine tax obligations and benefits

When hiring employees, you might be eligible for tax credits for R&D. Then there are also other credits to investigate, such as innovation loans, and all of the different taxes to consider. Determining your tax obligations and benefits requires looking at the full picture over a longer time span.

Focus on your strengths

Seeing the bigger picture is critical to setting yourself up for success. Be aware that to do this, you are dependent on many third parties, including a bookkeeper, controller, payroll personnel, CFO, and others. Why take on those headaches when your expertise lies within the science? Alternatively, you can outsource all of these responsibilities to one service provider, a one-stop shop, which will bring you more expertise for less time and money.

.jpg)